What Is Property And Casualty Insurance?

Property and casualty insurance, often called P&C insurance, is an umbrella term for policies that protect what you own and shield against personal liability claims. We’ll share the types of coverage available, how it works, and how much it costs. That way, you can make informed decisions when shopping for your policies.

Property insurance vs. casualty insurance

Property insurance and casualty insurance get bundled into one policy, but they cover different things. Property insurance can protect your belongings, residence, and vehicle if they are stolen or damaged by a covered peril. Casualty insurance, sometimes called liability insurance, covers medical, repair, and legal expenses should you accidentally cause injury to someone or damage their property.

Important note: Any insurance you purchase will have a policy limit, which is the maximum amount your insurer will pay out when you file a claim.

Types of property and casualty insurance

Here are some of the most common types of property and casualty insurance:

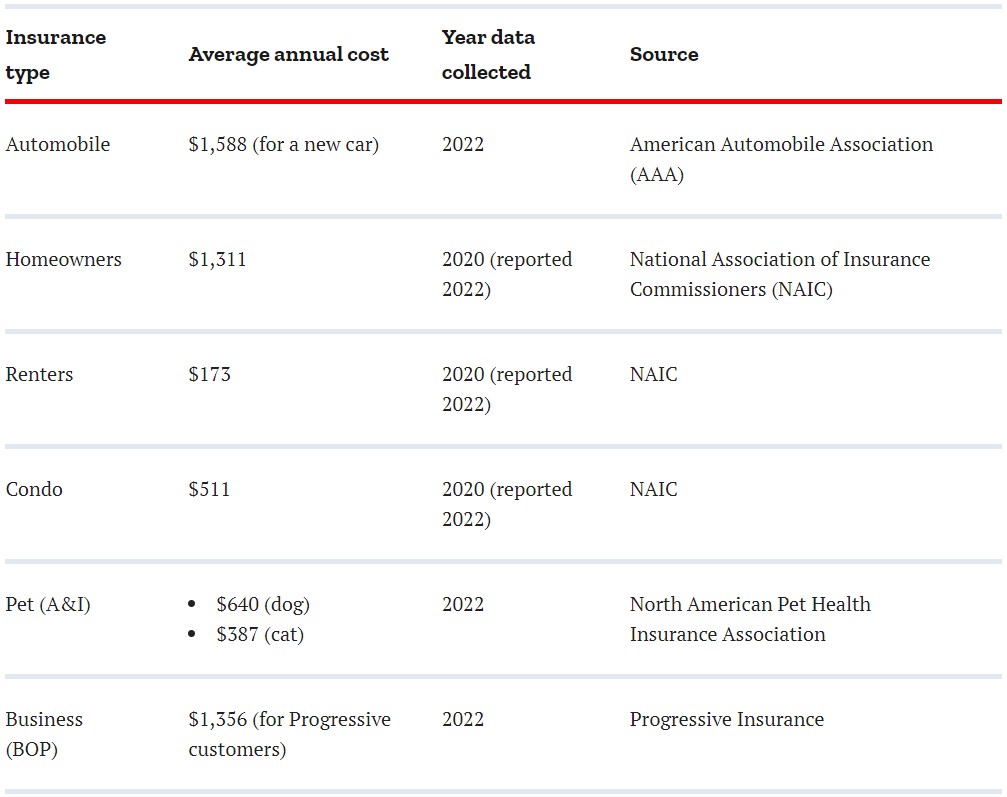

Automobile

Automobile insurance primarily covers costs associated with a car accident. For example, bodily injury liability and property damage liability pay out if you cause an accident that results in another person getting hurt or another party's car or property getting damaged. Collision coverage pays to repair your vehicle.

Homeowners

Homeowners insurance protects the structure of your house and the contents within it. It also has personal liability coverage. That way, if someone is hurt at your residence or their property gets damaged, you won’t have to pay out of pocket to cover their expenses. It also includes additional living expenses coverage, which pays for things like hotel stays and restaurant meals if your home is uninhabitable due to a covered event.

Renters

Renters insurance protects your personal belongings within the rented home, not the structure. Your landlord’s homeowners insurance policy is responsible for that. Like homeowners insurance, renters insurance features personal liability coverage that will pay out if another party sustains a covered loss while in your home. It also includes additional living expenses coverage.

Condominium

Condominium (condo) insurance protects your individual unit and personal belongings. However, the condominium association maintains a master insurance policy and is responsible for the overall structure of the building and the common areas, such as the swimming pool and hallways. Condo insurance also contains personal liability and additional living expenses coverage.

Pet

Pet insurance protects your animal companions. Accident-only (AO) insurance covers medical treatment required due to a covered accident, such as getting hit by a car or ingesting poison. Accident and illness (A&I) insurance covers accidents and ailments like infections or cancer.

Business

There are several types of business insurance, but a business owner's policy (BOP) is most like a property and casualty policy. It provides liability coverage if your business inadvertently harms someone or a customer gets injured on the company’s premises. It also protects the building from which you operate and the contents within it.

You may be required to obtain certain insurance. For example, in most states, you must have car insurance that meets a minimum standard. Plus, if you finance your vehicle, your lender will probably require you to maintain full coverage, including comprehensive and collision.

However, as long as you meet any minimum requirements imposed, property and casualty insurance can be customizable. For example, you can increase your deductible (how much you must pay before the insurance picks up the tab) to reduce your monthly premium.

Insurance can be complicated. It’s a smart idea to familiarize yourself with each type of policy's different protections before shopping for coverage.

What does homeowners property and casualty insurance cover?

Homeowners property and casualty insurance covers the building you live in (known as the dwelling) and your belongings inside. It also covers expenses associated with third-party liability claims for injuries or property damage sustained while at your residence. For example, homeowners insurance can protect you if your dog bites a guest or a delivery person slips on your icy outdoor stairs.

Your specific homeowners insurance policy coverage will depend on the level of protection you choose. There are three tiers available as follows:

- HO-1 (basic form): Provides the least coverage, only paying out for ten covered events (known as perils).

- HO-2 (broad form): Generally covers more perils than a basic form policy.

- HO-3 (special form): Provides the most protection, covering up to 16 types of perils. HO-3 is the most common type of homeowners insurance.

Perils your insurance may cover include:

- Water damage.

- Falling objects.

- Theft.

- Fire and smoke.

- Windstorms and hail.

- Lightning strikes.

- Weight of snow and ice.

- Vandalism.

- Malicious mischief.

- Damage from a vehicle.

- Explosions.

Your coverage will also depend on the add-ons you elect. For instance, you might opt for water and sewer backup coverage if you live in an area that floods. Or, if you own valuable fine jewelry, you may decide to get additional protection for those items.

You’ll also need to determine if you want replacement value or actual cost value (ACV) coverage for your home. Replacement coverage will pay for the cost of rebuilding your house (or replacing your items if you’re a renter). ACV coverage will only pay out the market value of your residence (or belongings), which may be significantly less than what it costs to replace it.

How does property and casualty insurance work?

With care and luck, you will never have an experience that requires you to file a property and casualty insurance claim. However, if you do, here are some general best practices to follow:

- Prioritize safety. For example, if your vehicle is in the middle of the street after an accident, walk over to the side of the road (if possible) before calling 9-1-1.

- Contact law enforcement (if necessary). You’d need to file a police report if your apartment got burglarized or get a copy of the accident report if you were in a car crash.

- Review your policy documents. Did you experience a covered event?

- Gather documentation. Take photos and videos of the damage. Write down what happened while it’s still fresh in your mind.

- Call your insurance company as soon as possible. Your policy may include a deadline to file a claim.

- Try to prevent further damage. For example, if a tree fell on your roof, lay a tarp over the hole to keep rainwater out of your home.

- Respond promptly. Act quickly on follow-up inquiries from your insurance company promptly and provide supporting documentation as requested.

Pro Tip: Estimate the damage before filing your claim. If you don’t think the cost to repair or replace the item will significantly exceed your deductible, it may make financial sense to pay out of pocket.

How much does property and casualty insurance cost?

Your property and casualty insurance cost will vary based on the type of policy you buy, the coverage you elect, your location, your deductible, your claims history, and other factors. However, we've gathered average cost data from the United States to give you an idea of what to expect:

If you want additional liability protection, consider purchasing an umbrella insurance policy. Umbrella insurance doesn’t replace your existing policies—it supplements them.

For example, let’s say you cause a car accident that results in $400,000 worth of property damage to the other party. Your auto insurance policy’s liability limit is $250,000. Fortunately, you have a $1 million umbrella insurance policy that can make up the difference.

Umbrella insurance is relatively inexpensive. According to Fidelity, you can generally purchase $1 million in coverage for under $500 per year.

Pro Tip: No matter which type of policy you decide to buy, compare quotes from several insurers to get the best deal possible.